Great stories always emerge at the beginning of the end of a bubble. This is mortgage fraud at its finest. Homeless people buying multiple properties! Is this just the tip of the iceberg? I'm speechless!

St. Petersburg Times - St. Petersburg, Fla.

Author: JEFF TESTERMAN

Date: Apr 9, 2006

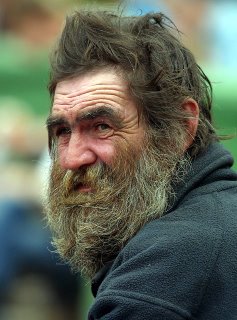

After struggling much of his adult life with unemployment, homelessness and drug addiction, Johnny Moon Sr. died last year on a dirty mattress on the floor of a small home near Tampa's College Hill district.

Moon, who looked far older than his 56 years, died of pneumonia brought on by malnutrition. He left behind a watch, a flashlight and a wallet containing a solitary dollar bill.

And more than a half-million dollars worth of real estate.

In the last months of his life, Moon left his signature scrawled on a variety of deeds and mortgages recorded at the Hillsborough County courthouse.

A high school dropout with no job history who got by on food stamps, Moon morphed into a real estate investor. Within a year, he bought five properties and signed for mortgages in excess of $614,000.

Moon appeared to be an astute picker of properties, finding value others did not see in Tampa's older neighborhoods. He paid well above market value yet managed to get loans to cover all, or nearly all, of the purchase price.

Three months before his death, Moon sold one home for $180,000 - $75,000 more than he paid 17 months earlier.

Those familiar with Moon's background have doubts about his abrupt transformation into real estate investor.

Linda Johnson, Moon's 59-year-old sister, a former packing plant worker who is disabled and lives in a mobile home in Tampa, thinks he was an unlikely candidate for easy credit.

"He never had nothing much, no bank accounts or nothing like that," she said.

Reading through Moon's probation record, Don Russell, division chief for the county probation department at the Salvation Army, concluded that Moon may have been used by someone else to front for real estate deals.

"If this guy walks into a bank with this background, they're not going to give him any kind of money," said Russell. "It looks like someone just used this man's name to get mortgage loans."

Evidence mounting since Moon's death suggests he may have been the latest straw man used in what the FBI says is a national epidemic of mortgage fraud.

In Tampa, one face behind the epidemic belongs to Matthew Cox, a mortgage broker suspected of using phony names, fake documents and forgery to defraud lenders of millions. He is now a fugitive sought on Secret Service warrants.

Cox was initially charged in 2001, accused of using a stolen identity to obtain loans on the home at 1904 E Powhatan Ave. Who was living there at the time?

None other than Johnny Moon Sr.

Among the four properties Moon bought in November 2003 was a white frame home at 2714 12th St. N in Ybor City. The seller was a land trust controlled by Chuong X. Dam, a Vietnamese businessman who was indicted by a federal grand jury in February on conspiracy and bank fraud charges. Dam is accused with others of using straw buyers to apply for fraudulent mortgage loans, though none of the charges involve the 12th Street home.

Records show Moon bought the 12th Street property from Dam's trust for $147,000 - triple what the county property appraiser said it was worth - and paid for it with a $147,000 mortgage loan.

The Federal National Mortgage Association, commonly called Fannie Mae, ended up with the home after Moon died and the loan went into foreclosure. For Fannie Mae, the loan has become a loser.

The lender's representatives discovered the 86-year-old home with the tin roof has leaks, flooring problems, no sink in the bathroom and no kitchen. As is, it is uninhabitable. The home is listed at $88,500, but so far, no takers.

Two businessmen who might provide insight into Moon's investment activities are his son, Johnny Moon Jr., and an associate, Dominic Ferrara. Both are licensed mortgage brokers who assisted Moon Sr. with his acquisitions, records show.

The younger Moon used a power of attorney form to sell one of his father's properties last year.

Ferrara witnessed and notarized that power of attorney, as well as deeds on sales executed by the elder Moon.

Ferrara also helped collect rent from tenants at one of the homes bought by Moon Sr., according to one renter.

"Mr. Dominic collected the $450 rent," said tenant Judy Vaughn, who with her husband and four children rented the four-bedroom home at 905 E 25th Ave. "He said it had to be cash. It was a good deal for us. The last place we were in was a shotgun shack."

The St. Petersburg Times contacted Moon Jr. and Ferrara to inquire about how the elder Moon had qualified for the mortgage loans, what had happened to the $75,000 profit on the home sale before Moon Sr.'s death, and why no one had stepped forward to claim an estate ownership in the real estate in Moon Sr.'s name, including three homes that eventually went into foreclosure.

Moon Jr. and Ferrara did not want to talk about it.

"My relationship with my father is personal," said Moon Jr. "It's none of your business."

"I don't know nothing about it," said Ferrara. "Please don't contact me again."

Moon Jr. and Ferrara are former business associates of Cox, the mortgage broker accused of fraud and now on the lam.

Cox, Moon Jr. and Ferrara worked together at a Tampa firm called Consortium Financial Services.

While there, Cox was charged with forgery and mortgage fraud after obtaining a $110,000 loan under an assumed name.

Moon Jr. and Ferrara were questioned after authorities discovered Cox had directed payments to them from the illegal proceeds totaling $45,000.

Moon Jr. and Ferrara told investigators they knew nothing about any illegal activity and believed they were simply helping hide money from Cox's wife. Neither Moon Jr. nor Ferrara was charged with any crime.

Moon Sr. served four stretches in prison, for delivery of heroin, possession of cocaine, aggravated assault and arson.

In all, he was arrested more than 30 times. Typically, he was assigned a public defender because he was indigent.

Charged with possession of marijuana in 1994, Moon Sr. told a judge he had no income, no cash, no assets.

Charged with shoplifting a can of tuna and a package of steak from a Winn-Dixie in 1998, Moon Sr. testified he received $494 in Social Security income and had last worked "18 years ago."

"He had a long battle with prescription drugs," said Anjeanette Moon, a former daughter-in-law. "He was homeless a lot of the time."

Then came the real estate career.

In November 2002, Moon Sr. signed for an $85,000 loan to buy the home at 2204 E Chipco St.

Six days later, Moon was arrested at a Publix supermarket on Nebraska Avenue after stuffing packages of razor blades, Tylenol and Advil tablets into his pocket and trying to leave without paying. He was charged with petty theft.

Moon pleaded no contest to the $26.69 theft and got 60 days in jail and six months' probation.

Probation records show he reported receiving $108 a month in food stamps and $555 a month from Supplemental Security Income - a form of disability income generally available to people owning less than $2,000 in property.

A few months after being released and reporting that meager income, Moon Sr. signed for four mortgage loans, totaling $529,300, to buy four more properties. The four purchases occurred in a two- week period.

He somehow got himself to all four closings, records show, and presented a Florida driver's license as identification, though the state had revoked his license indefinitely during the 1990s when he was classified as a habitual traffic offender.

Two weeks after Moon Sr.'s flurry of purchases, Moon Jr. and Ferrara paid $53,000 for a two-bedroom home with a fenced yard at 3309 E Dr. Martin Luther King Jr. Blvd.

In July 2005, Moon Sr.'s body was found in one of the back bedrooms there.

Five months after the death, Moon Jr. and Ferrara sold the small home for $98,000 - $45,000 more than they paid for it.

Times researcher Cathy Wos contributed to this report. Jeff Testerman can be reached at (813) 226-3422 or testerman@sptimes.com.

POOR MAN, RICH MAN?

Oct. 7, 1948: Johnny Moon Sr. born, the son of a Baptist minister. He will drop out of high school and work briefly as a carpet installer. During his adult lifetime, he will be arrested more than 30 times.

1977-1989: Served four stretches in prison, for convictions for heroin, cocaine, arson and assault.

June 1998: Charged with shoplifting a can of tuna and a steak from Winn-Dixie. Told judge he had no assets, last worked 18 years ago and subsisted on Social Security income of $494 a month. Sentenced to 45 days in jail.

Nov. 5, 2002: Signed for an $85,000 mortgage loan to purchase home at 2204 E Chipco St. for $85,000.

Nov. 11, 2002: Charged with shoplifting headache tablets and razor blades from Publix. Sentenced to 60 days in jail. Arresting officers list his address as "at large."

Feb. 26, 2003: Released from jail, reported to probation. Said he gets $505 a month in Supplemental Security Income and $108 a month in food stamps.

Nov. 7, 2003: Signed for two mortgage loans: $150,100 to buy the home at 905 25th Ave. E for $158,000, and $137,700 to buy the home at 3801 N Dartmouth Ave. for $153,000.

Nov. 14, 2003: Signed for $147,000 mortgage loan to buy the home at 2714 12th St. N for $147,000.

Nov. 21, 2003: Signed for a $94,500 mortgage loan to buy the home at 1410 31st Ave. E for $105,000, the fourth home he bought that month. Total mortgages: $529,300.

April 27, 2005: Sold home at 1410 31st Ave. E for $180,000 - $75,000 more than he paid 17 months earlier.

July 30, 2005: Died of pneumonia due to malnutrition. Police found meager personal effects, including a single dollar bill in his wallet. His real estate later goes into foreclosure after no relatives come forward to establish an estate for him.